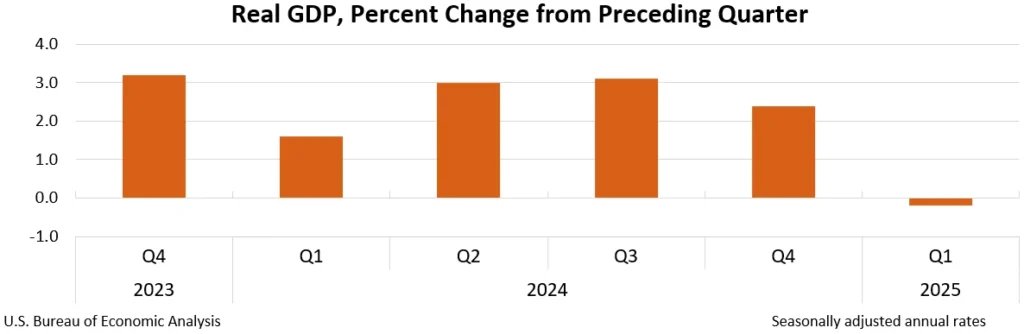

U.S. real GDP declined by 0.2% in Q1 2025 – the revised BEA estimate highlights the impact of Trump-era tariffs and the broader U.S. economic strategy. This marks the first contraction since early 2022 and a sharp reversal from the 2.4% growth recorded in the fourth quarter of 2024, driven by reduced government spending and increased imports, partially offset by gains in investment and exports.

Data Revision and GDP Contraction Structure

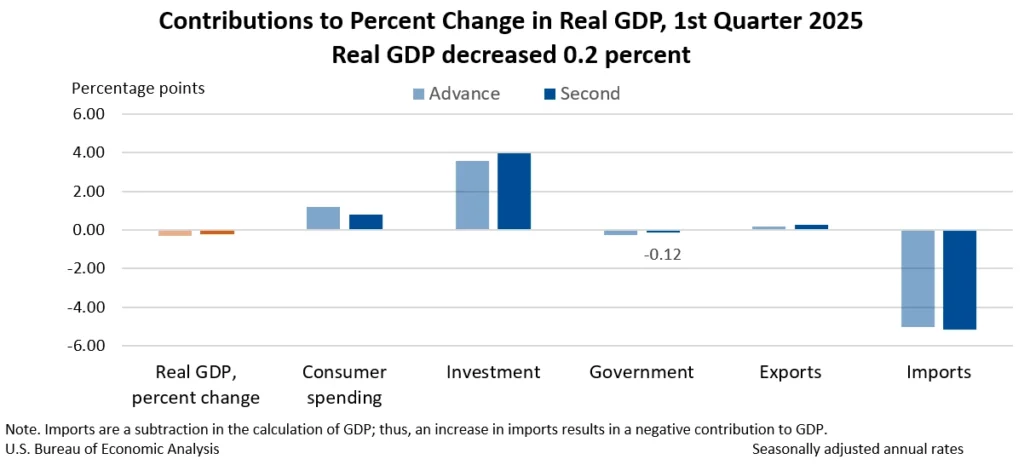

Geopolitical uncertainty and the tariff war generated plenty of bold statements, but now we have the numbers. Compared to the initial estimate, the GDP figure was revised up by 0.1 percentage points but remained negative, with the main contribution to the contraction of the U.S. economy in Q1 2025 coming from increased import volumes – a factor that, under BEA methodology, is subtracted in GDP calculation.

Additional negative impacts came from reduced consumer spending and government investment, while exports and private investment had a positive effect, both revised upward. In particular, investment growth offset part of the decline, while government spending decreased, deepening the overall downturn.

Income, Spending, and Price Dynamics

Real final sales to domestic purchasers – including consumer spending and capital investment – rose by 2.5%, which is 0.5 percentage points lower than in the previous estimate. At the same time, real gross domestic income (GDI) fell by 0.2%, in contrast to the 5.2% growth in Q4 2024.

All this occurred against the backdrop of persistently high inflation: the price index for gross domestic purchases rose by 3.3%, and the core PCE price index (excluding food and energy) by 3.4%, reflecting a moderate 0.1 percentage point downward revision from the previous estimate.

A key factor here is the decline in profits from current production, which dropped by a notable $118.1 billion, compared to an increase of $204.7 billion in Q4. This is already a direct effect of tariffs and points to weakening corporate sector earnings amid declining demand and a possible revaluation of inventory levels.

Conclusion

The 0.2% decline in U.S. real GDP in Q1 2025 is now confirmed, and alongside the drop in GDI and corporate profits, it indicates a notable weakening of economic activity.

At the same time, inflation remains persistently high, especially in PCE components, which may be a signal of the potential start of a slowdown phase – particularly in the context of declining consumer spending and reduced government investment.

In many ways, this represents the transitional period previously mentioned by Trump, along with the inevitable effects that accompany it against a backdrop of already heightened international tensions and economic uncertainty.